Dealing with a water leak in your home can be overwhelming, and knowing how to handle the insurance claim can make a big difference in your recovery process. You might wonder when it’s the right time to file a water leak insurance claim, what damages are covered, or how to avoid common pitfalls that lead to claim denials.

This guide will walk you through everything you need to know to make a successful water leak insurance claim—helping you protect your home and your wallet. Keep reading to learn how to take control of your situation and get the support you deserve.

Water Leak Coverage Basics

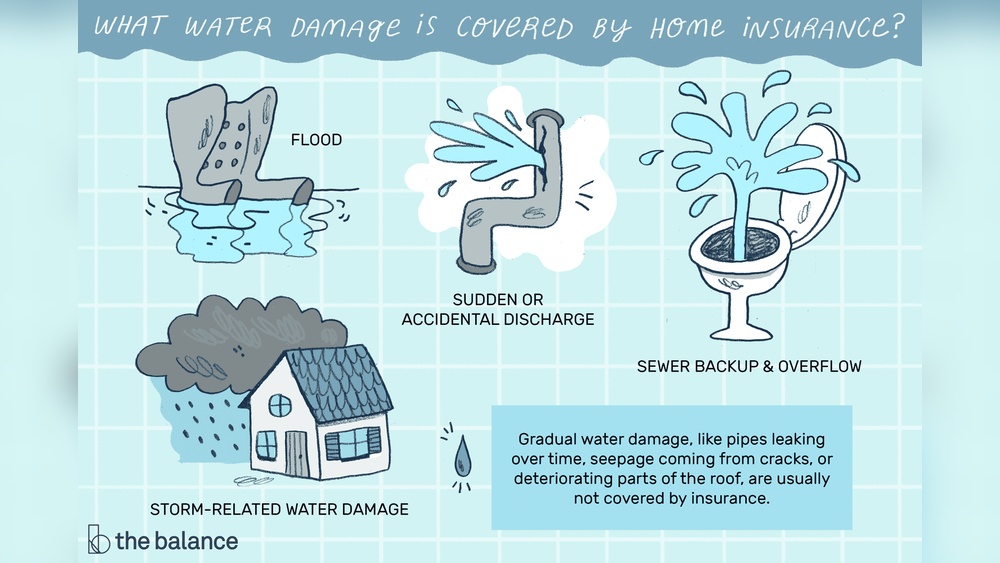

Types of water leaks covered often include sudden and accidental events. Examples are burst pipes, toilet overflows, or broken washer hoses. These leaks cause immediate damage and are usually covered by insurance policies.

Damage from gradual leaks or wear and tear usually is excluded. Insurance companies expect homeowners to maintain their property to prevent slow leaks. Sudden damage claims are easier to approve than gradual ones.

| Type of Leak | Coverage |

|---|---|

| Sudden Leaks | Typically covered (burst pipes, toilet overflow) |

| Gradual Leaks | Usually excluded (slow leaks, wear and tear) |

| Common Exclusions | Maintenance issues, flooding from outside, sewer backup (unless added) |

Insurance policies often exclude damage caused by lack of maintenance. Flood damage or sewer backups need special coverage. Understanding these limits helps when filing a claim.

Preparing For Your Claim

Fix the leak quickly to prevent more damage. Shut off the water supply right away. Call a plumber if needed to stop the leak.

Document damage thoroughly with photos and videos. Take pictures from different angles. Keep receipts for any repairs or replacements.

Estimate repair costs by getting written quotes from contractors. Compare prices and save all estimates. This helps when you file your claim.

Filing Your Insurance Claim

Notify your insurance company as soon as possible after discovering a water leak. Provide clear details about the incident, including when and where it happened. This helps start the claim process quickly and smoothly.

Gather and submit all necessary evidence. Take photos or videos of the damage and the source of the leak. Keep receipts for any repairs or temporary fixes you make. This proof supports your claim and speeds up approval.

Work closely with the insurance adjuster assigned to your case. They will visit your home to inspect the damage. Answer their questions honestly and provide any extra information they need. This cooperation helps ensure a fair assessment and payout.

Maximizing Your Payout

Policy limits define the maximum amount your insurer will pay. Check your water damage coverage carefully. Some policies exclude certain types of leaks or have sub-limits for water damage. Know your deductible, as it affects your payout. Understanding these details helps avoid surprises during claims.

Negotiating with insurers means being clear and calm. Provide photos, receipts, and repair estimates to support your claim. Don’t accept the first offer if it seems low. Ask for a re-evaluation or provide extra proof to increase your payout.

Hiring a public adjuster can help if your claim is complex or disputed. They work for you, not the insurance company. Public adjusters know how to read policies and spot missed damages. Their fee is usually a percentage of your final payout, but their help often results in a higher settlement.

Common Reasons Claims Are Denied

Gradual damage and wear often cause claim denials. Insurance covers sudden leaks, not slow leaks over time. Damage from long-term leaks is seen as maintenance issues.

Insufficient documentation can stop claims. Take photos and keep receipts of repairs. Detailed proof helps show the damage was sudden and accidental.

Policy exclusions list what is not covered. Some policies exclude water damage from floods or sewer backups. Check your policy carefully before filing.

Handling Mold And Secondary Damage

Mold coverage depends on your insurance policy and the cause of the leak. Most policies cover mold only if it results from a sudden, accidental water leak like a burst pipe. Mold caused by long-term leaks or neglect usually is not covered. Always check your policy details for specific mold coverage limits.

Stopping further damage is crucial. Turn off the water source immediately. Dry wet areas using fans or dehumidifiers. Remove soaked carpets and furniture to prevent mold growth. Acting fast can reduce repair costs and insurance claims.

For cleanup and restoration, hire professionals if damage is extensive. Use protective gear during cleanup to avoid health risks. Clean hard surfaces with mold-killing solutions. Dispose of items that are too damaged to save. Document all damages and repair expenses for your insurance claim.

Legal And Financial Considerations

Deductibles are the amount you pay before insurance helps. Check your policy to know your deductible. Sometimes, small leaks cost less than the deductible, so claims might not pay off.

Consulting an attorney helps if your claim is denied or if there is a dispute. An attorney can explain your rights and guide you through the process. They can also help with complex cases or large losses.

| Financial Assistance Options | Description |

|---|---|

| Emergency Funds | Use savings or emergency money to cover urgent repairs quickly. |

| Loans | Home improvement loans or personal loans can help pay for repairs. |

| Government Aid | Some programs provide help after serious water damage or disasters. |

Frequently Asked Questions

How Do I Make A Successful Water Leak Insurance Claim?

Report the leak promptly to your insurer. Document damage with photos and receipts. Fix the leak quickly to prevent more damage. Provide clear, honest details about the incident. Keep records of all communications and repairs to support your claim.

Who Is Responsible For Paying For A Water Leak?

The property owner usually pays for water leak repairs. Homeowners insurance may cover sudden, accidental leaks. Gradual leaks often aren’t covered.

What Kind Of Water Leaks Are Covered By Insurance?

Insurance covers sudden, accidental water leaks like burst pipes, overflowing toilets, or broken appliance hoses. Gradual leaks or wear and tear usually are not covered. Always document damage and repair promptly to support claims.

Why Would Insurance Deny A Water Damage Claim?

Insurance may deny water damage claims if the damage results from gradual leaks, poor maintenance, or wear and tear. Claims often require sudden, accidental water events like burst pipes for coverage. Lack of proper documentation or failure to repair the source promptly can also lead to denial.

Conclusion

Water leak insurance claims need quick and clear action. Document all damage carefully and contact your insurer promptly. Know your policy’s coverage limits and deductible before filing. Sudden leaks often qualify for coverage, unlike slow leaks. Repair the leak quickly to prevent more damage and costs.

Understanding the claim process helps avoid delays and denials. Stay organized with photos, receipts, and communication records. Protect your home by acting fast and staying informed.

Read More

- Claim Bridge Settlement Support: Expert Tips to Maximize Your Claim

- Insurance Claim Review Service: Maximize Your Settlement Today

- Property Damage Claim Estimate: Maximize Your Compensation Today

- Fast Accident Claim Assistance: Get Quick, Stress-Free Help Today

- Claim Settlement Strategy Guide: Expert Tips for Fast Approval

- Insurance Litigation Attorney Help: Win Your Claim with Expert Guidance

- Settlement Counsel Case Review: Expert Insights for Winning Results

- Claim Lawyer Consultation Online: Expert Advice at Your Fingertips

- Claim Dispute Legal Support: Expert Help for Winning Cases

- Long Term Care Injury Claim: Maximize Your Compensation Now